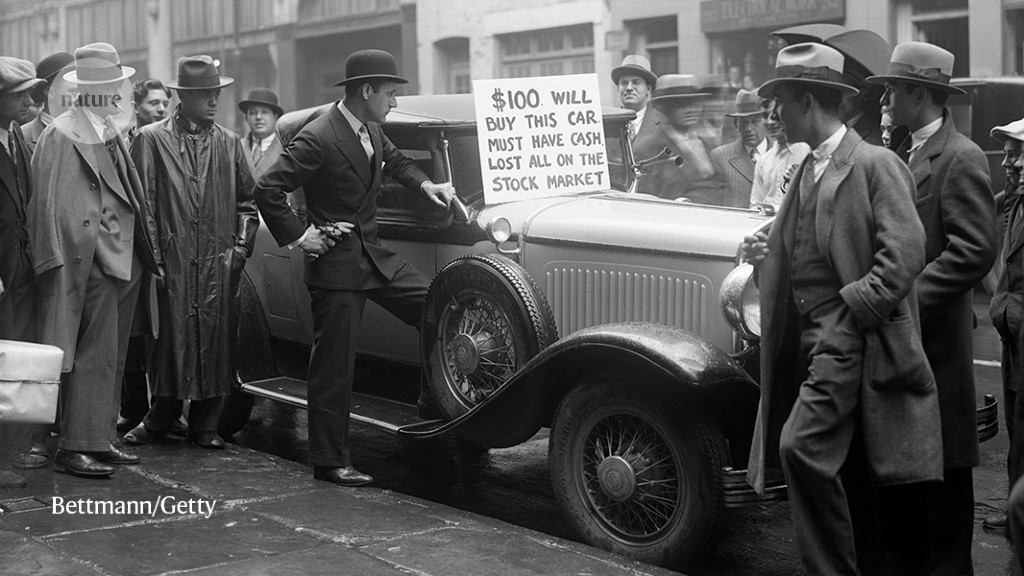

A Wall Street speculator trying to sell his car.Credit: Bettmann/Getty

Seven Crashes: The Economic Crises That Shaped Globalization Harold James Yale Univ. Press (2023)

In the mid-1920s, the mood in the United States was buoyant. After years of surging economic growth, fuelled by expansion in the automobile industry and speculation in financial markets, the United States had the lowest debt of any large industrial nation. The future looked just as rosy. A 1926 article in The Wall Street Journal noted how “American wealth has doubled in the past dozen years”, delivering “a rate of progress that has never been known in Europe”.

That astonishing uptick was real. Yet the exuberant mood vanished just a few years later with the stock-market crash of October 1929, followed by a wave of bank failures. As the trouble spread to Europe, more banks succumbed, and the world entered the Great Depression. But the seeds of this downturn were evident even during the boom. US authorities worried over how financial innovations — including the invention of derivative contracts such as options — had created a vast network of overextended investors engaging in risky speculation.

What was so new — and had for a time seemed so beneficial — led instead to profound upheaval and a global social and economic crisis.

How mathematics stopped being defined by reality — and started to invent new ones

Similar events, historian Harold James argues in his illuminating book Seven Crashes, recur across human history. Sudden outbursts of novelty presage most major economic crises. As James relates, when economist Joseph Schumpeter asked the question “how do things become different?”, the answer was: “when something fundamentally new occurs in the world, we are confronted by an enigma.”

Such occurrences, which have had a decisive role in shaping economic history, are not normal or predictable, James argues. The origin of each crisis was an economic or social ‘shock’: a famine, as was the case in 1840s Europe; a global energy shortage, as happened in the 1970s; or a global pandemic in the case of COVID-19. The outcome, James argues, is often an immediate retreat from globalization, as nations close in on themselves, seeking safety and stability. Yet, simultaneously, there is also a push for greater globalization, stemming from the emergence of new technologies or the search for fresh resources.

James examines seven historic crises. For example, during the European agrarian crisis of the 1840s, bad weather and crop failures — caused in particular by potato blight — led to widespread starvation. From Ireland to Germany, prices of potatoes, rye and wheat doubled over a few years. Millions of people died from hunger and disease brought on by malnutrition.

This misery caused nations to hoard supplies, but also to push for more global trade. In just a few years, France increased its grain imports more than tenfold. Other countries responded by using new forms of international credit and governing institutions, with public authorities taking closer control of the economy and trade. New kinds of business emerged, including the limited liability joint-stock company, which encouraged risky enterprises by protecting investors from full liability for their activities.

The Great Depression evoked a similar response. As James notes, the economic decline after 1929 convinced many that the world was witnessing ‘the end of capitalism’. In a 1933 radio address, US president Franklin Roosevelt argued for a return to nationally focused economies that were not subject to the “old fetishes of so-called international bankers”. British economist John Maynard Keynes greeted this language approvingly. In his landmark 1936 book, The General Theory of Employment, Interest and Money, Keynes criticized the instability inherent to international speculative finance and argued for state planning and control of the monetary system.

Did the Black Death break feudalism and make capitalism? Maybe, maybe not

Yet, from this temporary move away from globalization emerged the Bretton Woods agreement in 1944, which established an international system of currency exchange and the International Monetary Fund, a financial agency of the United Nations. The agreement was decisive in furthering globalization by allowing for safer and more-predictable flows of capital for international investments.

James also considers the financial crash of 1873 in Europe and North America, the upheaval of the First World War, inflation in the 1970s and the global recession of 2008. In such circumstances, he writes, “the radical character of the shock spurred a search for alternatives: new products but also new mechanisms to move goods”.

During the 1970s, for example, soaring inflation — exacerbated by energy shortages linked to political instability in the Middle East — stimulated a push for energy efficiency and alternative energy sources. In the United States, business-friendly Republican president Richard Nixon was the unlikely agent in introducing energy-saving measures such as a reduced national speed limit, higher fuel-efficiency standards and an encouragement to turn down home thermostats.

Similar pleas for public-spirited shifts in behaviour were at the centre of the global response to the COVID-19 pandemic. This crisis, James notes, was a product of globalization and the connections that enabled the virus SARS-CoV-2 to spread so rapidly. Yet the challenge was also fought with worldwide sharing of science, technology and learned best practices.

One outcome of the pandemic, James argues, was a broad push for bigger and more effective government, following from the chaotic but ultimately effective deployment of rapidly developed vaccines, as well as the support that helped to preserve social function. The economic shock of the pandemic was not only the loss of economic output brought on by social restrictions, but acute shortages of products — foods, medicines, semiconducting chips — caused by disrupted supply lines. The world is still living with the consequences, in the form of inflation linked to the shortages, which was amplified by rising energy prices after Russia invaded Ukraine in 2022.

Is ‘speciesism’ as bad as racism or sexism?

Responses to these challenges will emerge in the next stage of the continual push–pull of the socio-economic process. If the rise of populist movements around the globe reflects a backlash against globalization, and a yearning to return to isolationist nation states, there’s an equal demand from many people for greater coordination on the international level — to help to avoid another pandemic, or to forge a better response to the problems of climate change as they grow more severe.

It is a fascinating idea that many of humanity’s greatest achievements have, ultimately, come as responses to times of crisis, which bring suffering and present deep conceptual problems. That said, James relies rather heavily on the concept of an economic shock — a surprising or unpredictable event that drives big changes. He sidesteps the question of how to identify which ones count as shocks, and whether these shocks really caused specific events. But this problem plagues any causal analysis of historical occurrences. Subtler trends and feedbacks, such as narratives that spread slowly and largely invisibly among people until they cause shifts in behaviour, might be just as important, if harder to see.

That quibble aside, James’s analysis is persuasive, and his book offers an illuminating history of how our world became so globalized. Not as the result of an inexorable process, but by jerking along an erratic and haphazard path towards a more unified economy.

More News

Author Correction: Stepwise activation of a metabotropic glutamate receptor – Nature

Changing rainforest to plantations shifts tropical food webs

Streamlined skull helps foxes take a nosedive